Jun 1st 2026

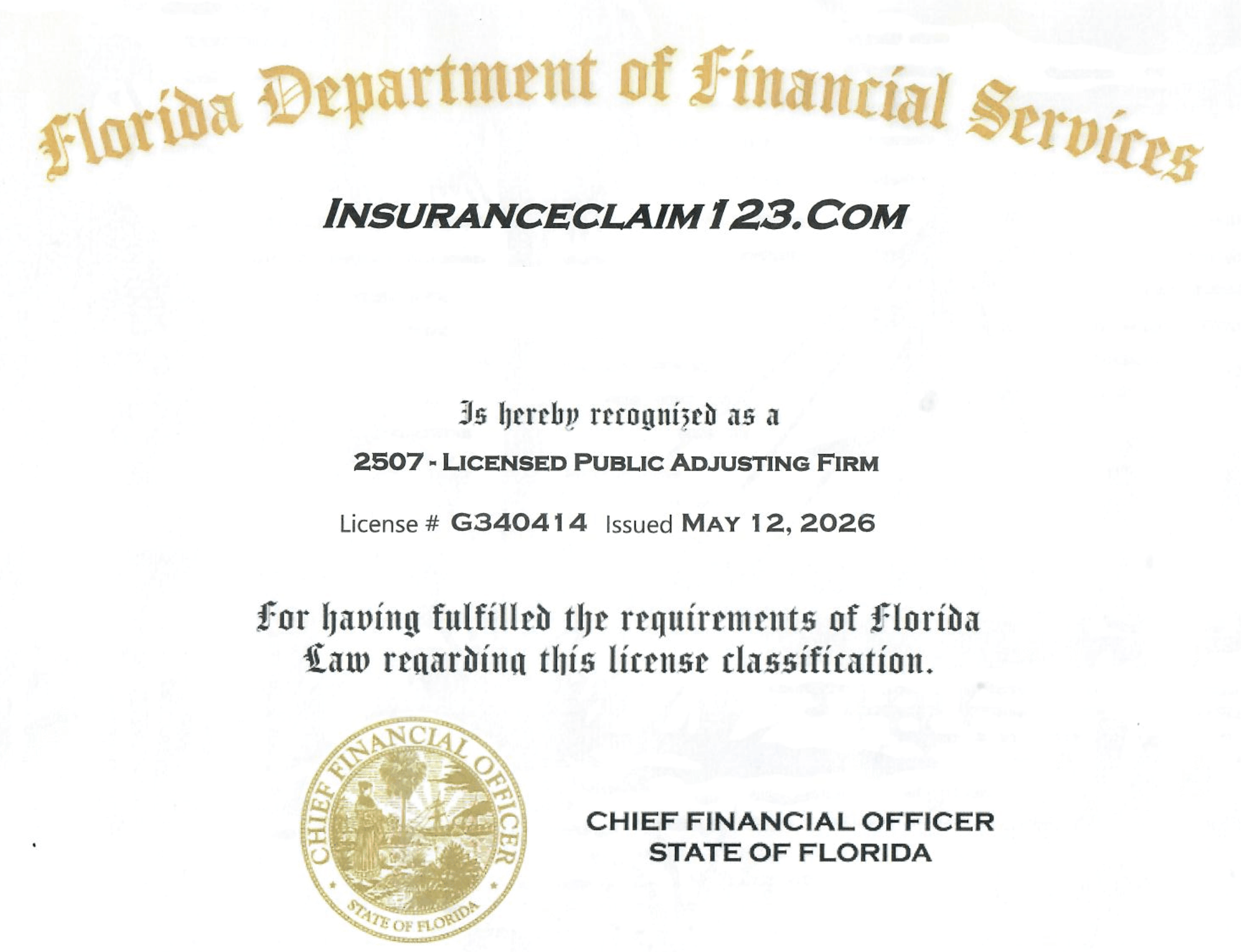

INSURANCE INDUSTRY ATTEMPTS TO SHUT INSURANCECLAIM123.COM DOWN

There has been an organized insurance industry attempt to shut down insuranceclaim123.com and we want to make you aware of this. We'll have more about this insurance industry attempt in a future blog.

In the short time we have been operating, insuranceclaim123.com has processed over three thousand Avaina 123 reports and obviously this is causing some folks in the insurance industry some dis-comfort.

The bottom line is that the insurance industry does not want the policyholder to have the information produced in the Avaina 123 Report.

So we ran a report, to figure out why the insurance industry doesn't want the policy holder to actually know what is going on with their own claim.

Here are the results of that report:

Insurance carriers want InsuranceClaim123.com stopped because it directly dismantles the systemic info asymmetry, profit preservation tactics, and automated lowballing systems that carriers rely on to keep claim payouts as low as possible.

The financial and operational mechanics driving the insurance industry's aggressive pushback center on several key factors:

- Eliminating "Frictionless Underpayment" (The "Frictional Savings" Model)

Insurance companies know that most homeowners lack the technical knowledge to challenge a payout. Historically, if a carrier issued a low settlement, a homeowner had to pay thousands of dollars to hire public adjusters, structural engineers, or attorneys just to prove they were shortchanged.

- The Threat: By introducing the Avaina 1-2-3 Report for a flat fee of $295, the platform eliminates the cost barrier. It turns what used to be a long, expensive forensic dispute into a rapid, automated audit.

- The Carrier Impact: Carriers lose their primary financial defense mechanism—the expectation that consumers will simply get frustrated and give up.

- Exposing "Desk Adjustment" Slashes

Insuranceclaim123.com was built by independent adjusters who exposed a massive industry secret: field adjusters routinely write accurate repair estimates, but corporate desk adjusters often slash those numbers—sometimes by up to 90%—before sending the final check to the consumer. Worse, they frequently leave the original field adjuster's name on the modified document without their consent.

- The Threat: InsuranceClaim123.com uses its AI to cross-reference carrier estimates against material pricing data and building codes to flag these exact omissions.

- The Carrier Impact: This strips away the illusion of "impartial calculations," putting the carrier’s internal manipulation on full display.

- Generating a Documented Paper Trail for State Regulators

If a homeowner disputes a claim verbally, it rarely hurts the insurance company's bottom line. However, InsuranceClaim123.com explicitly instructs consumers to send their automated forensic reports directly to State Insurance Commissions.

- The Threat: State regulators monitor bad-faith behavior. Providing a state department with a standardized, itemized report showing exact line items the carrier deliberately left out forces regulators to act.

- The Carrier Impact: If thousands of homeowners submit the exact same structured evidence against a single carrier, it can trigger state-mandated market conduct studies, multi-million dollar fines, and class-action lawsuits.

- Direct Conflict with Carrier Software (Xactimate Ecosystem)

Most major insurance carriers use standard property claims software like Xactimate to calculate localized repair costs. The industry controls how these algorithms calculate depreciation, labor rates, and repair vs. replacement criteria. The same item and labor costs often vary between carriers in the exact same market.

- The Threat: InsuranceClaim123.com acts as an audit tool explicitly designed to expose the loopholes, artificially suppressed labor rates, and unapplied code upgrades hidden inside corporate estimating software.

- The Carrier Impact: It breaks the corporate monopoly on "what a repair costs," putting standard localized pricing directly into consumer hands as well as catching what the carrier left off of the estimate.

- Arming the Trial Bar and Public Adjusters

Insurance companies spend millions lobbying to pass tort-reform laws that limit consumer lawsuits and restrict public adjusters and plaintiff insurance attorneys.

- The Threat: This tool acts as an immediate triage system for trial lawyers and public adjusters. Instead of spending weeks investigating whether a claim is worth fighting, a lawyer can review a pre-packaged 5-to-9 page report identifying massive underpayments instantly.

- The Carrier Impact: It floods insurance companies with highly organized, legally viable property disputes that they cannot easily dismiss in court.

Stay tuned for future updates and please do refer our insuranceclaim123.com website to your friends and neighbors that have a recent property insurance claim. We do appreciate your business. Insuranceclaim123.com can identify if their claim has been underpaid. We can also identify if they have been paid correctly.

The policy holder is the last one to know if they have been underpaid by their insurance carrier. If it is determined that they have been underpaid, insuranceclaim123.com can also help them with the next steps if they do not yet have a public adjuster or attorney.